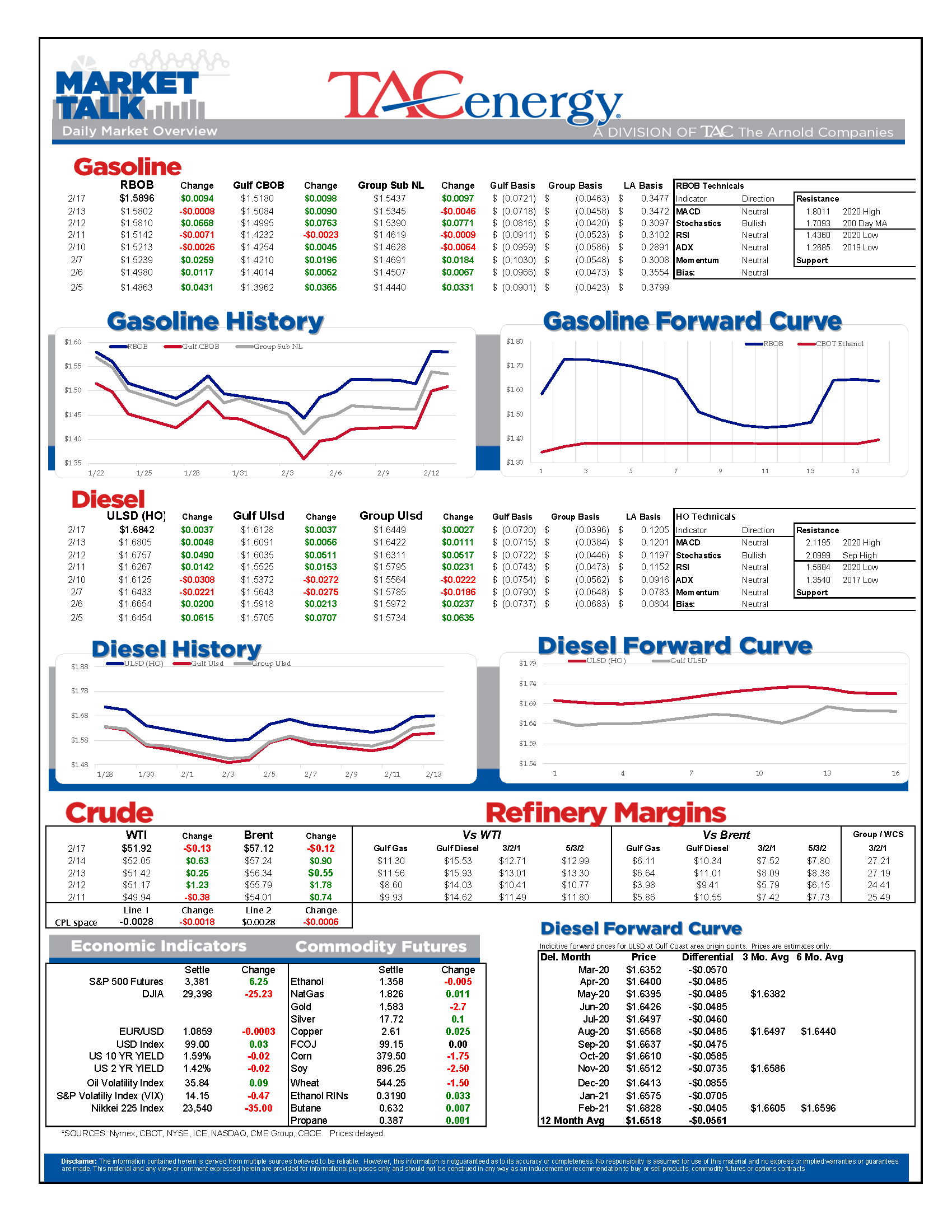

Abbreviated Trading Session Starts Mixed

Energy futures are starting Presidents’ Day abbreviated trading session mixed this morning. The prompt month gasoline contract is up about a penny per gallon, while its distillate counterpart is down about the same. American and European crude oil benchmarks are pretty much flat so far, sitting on opposite sides of unchanged.

The two-week fire sale of WTI longs by the money manager category of commodities traders slowed last week with the liquidation of just over 9,000 contracts. It looks like the fun is only getting started for Brent crude however, as this week’s drop in speculative longs breaks through the five-year seasonal average. It will be interesting to see if the liquidation slows as it reaches the low end of the seasonal range, like WTI did this week, or if the risk-off mentality will draw new lows on the chart.

Baker Hughes reported the addition of two working oil rigs last week. Despite the sizable drop in WTI prices, last week’s number brings the total net change in rig count to +8 since the beginning of the year. While demand concerns related to the Wuhan virus still seem to loom over producers, there seems to be a light at the end of the tunnel as some start to ask ‘what happens next?’

Click here to download a PDF of today's TACenergy Market Talk.

Latest Posts

Gasoline Futures Are Leading The Way Lower This Morning

The Sell-Off Continues In Energy Markets, RBOB Gasoline Futures Are Now Down Nearly 13 Cents In The Past Two Days

Week 15 - US DOE Inventory Recap

Prices To Lease Space On Colonial’s Main Gasoline Line Continue To Rally This Week

Social Media

News & Views

View All

{kind=link}

Gasoline Futures Are Leading The Way Lower This Morning

It was a volatile night for markets around the world as Israel reportedly launched a direct strike against Iran. Many global markets, from equities to currencies to commodities saw big swings as traders initially braced for the worst, then reversed course rapidly once Iran indicated that it was not planning to retaliate. Refined products spiked following the initial reports, with ULSD futures up 11 cents and RBOB up 7 at their highest, only to reverse to losses this morning. Equities saw similar moves in reverse overnight as a flight to safety trade soon gave way to a sigh of relief recovery.

Gasoline futures are leading the way lower this morning, adding to the argument that we may have seen the spring peak in prices a week ago, unless some actual disruption pops up in the coming weeks. The longer term up-trend is still intact and sets a near-term target to the downside roughly 9 cents below current values. ULSD meanwhile is just a nickel away from setting new lows for the year, which would open up a technical trap door for prices to slide another 30 cents as we move towards summer.

A Reuters report this morning suggests that the EPA is ready to announce another temporary waiver of smog-prevention rules that will allow E15 sales this summer as political winds continue to prove stronger than any legitimate environmental agenda. RIN prices had stabilized around 45 cents/RIN for D4 and D6 credits this week and are already trading a penny lower following this report.

Delek’s Big Spring refinery reported maintenance on an FCC unit that would require 3 days of work. That facility, along with several others across TX, have had numerous issues ever since the deep freeze events in 2021 and 2024 did widespread damage. Meanwhile, overnight storms across the Midwest caused at least one terminal to be knocked offline in the St. Louis area, but so far no refinery upsets have been reported.

Meanwhile, in Russia: Refiners are apparently installing anti-drone nets to protect their facilities since apparently their sling shots stopped working.

Click here to download a PDF of today's TACenergy Market Talk.

The Sell-Off Continues In Energy Markets, RBOB Gasoline Futures Are Now Down Nearly 13 Cents In The Past Two Days

The sell-off continues in energy markets. RBOB gasoline futures are now down nearly 13 cents in the past two days, and have fallen 16 cents from a week ago, leading to questions about whether or not we’ve seen the seasonal peak in gasoline prices. ULSD futures are also coming under heavy selling pressure, dropping 15 cents so far this week and are trading at their lowest level since January 3rd.

The drop on the weekly chart certainly takes away the upside momentum for gasoline that still favored a run at the $3 mark just a few days ago, but the longer term up-trend that helped propel a 90-cent increase since mid-December is still intact as long as prices stay above the $2.60 mark for the next week. If diesel prices break below $2.50 there’s a strong possibility that we see another 30 cent price drop in the next couple of weeks.

An unwind of long positions after Iran’s attack on Israel was swatted out of the sky without further escalation (so far anyway) and reports that Russia is resuming refinery runs, both seeming to be contributing factors to the sharp pullback in prices.

Along with the uncertainty about where the next attacks may or may not occur, and if they will have any meaningful impact on supply, come no shortage of rumors about potential SPR releases or how OPEC might respond to the crisis. The only thing that’s certain at this point, is that there’s much more spare capacity for both oil production and refining now than there was 2 years ago, which seems to be helping keep a lid on prices despite so much tension.

In addition, for those that remember the chaos in oil markets 50 years ago sparked by similar events in and around Israel, read this note from the NY Times on why things are different this time around.

The DOE’s weekly status report was largely ignored in the midst of the big sell-off Wednesday, with few noteworthy items in the report.

Diesel demand did see a strong recovery from last week’s throwaway figure that proves the vulnerability of the weekly estimates, particularly the week after a holiday, but that did nothing to slow the sell-off in ULSD futures.

Perhaps the biggest next of the week was that the agency made its seasonal changes to nameplate refining capacity as facilities emerged from their spring maintenance.

PADD 2 saw an increase of 36mb/day, and PADD 3 increased by 72mb/day, both of which set new records for regional capacity. PADD 5 meanwhile continued its slow-motion decline, losing another 30mb/day of capacity as California’s war of attrition against the industry continues. It’s worth noting that given the glacial pace of EIA reporting on the topic, we’re unlikely to see the impact of Rodeo’s conversion in the official numbers until next year.

Speaking of which, if you believe the PADD 5 diesel chart below that suggests the region is running out of the fuel, when in fact there’s an excess in most local markets, you haven’t been paying attention. Gasoline inventories on the West Coast however do appear consistent with reality as less refining output and a lack of resupply options both continue to create headaches for suppliers.